Have you considered Rental Vacancy, Type of Asset or Cash Flow?

Some things you must consider in your property investment journey are rental vacancy, the type of asset you are investing in and budgeting and cash flow.

Rental Vacancy

If you do not have a tenant, it is nearly impossible for most people to hold the property long term. A bit of local research will determine how long it will take to rent a property, how much you should achieve for it and what the local area vacancy rate is. With Property Management there tends to be one or two area specialists that set the highest standard; determine where you will get the best service which should come far before just the best price.

If you call a property manager as an investor you will often get one set of answers -they up-sell you. If you call as a prospective tenant looking for a residence you get a second set of answers, they “manage your expectations“!

The amount you can bank on is usually somewhere in the middle.

When you find a good property manager, treat them with the utmost respect – they are gold! You want to make your property investment experience as hands off and hassle free as possible.

They have their finger on the local pulse and know how and when to increase rental expectations. They can take care of the small day to day running issues of your property, allowing you to focus on the more important things in life.

Type of Asset

Apartment, Townhouse, House? The age old question.

Quite often it comes down to land value. For a similar price you can own a 1 bed CBD apartment, a 2 bed inner ring apartment, a middle ring townhouse, a detached house in the outer growth corridor. As previously discussed, it is not necessarily the largest block of land that wins, but where land is in the major growth phase. An apartment may have very little land value however if there is short supply of apartments in the area then the “land value” of the apartment will increase. As we see higher density living in our capital cities, a detached house on a block of land will become a premium asset class.

When you build a portfolio I would suggest that you diversify through the assets. This gives the ability to have an asset running hot at the same time that other assets are in a moderate phase.

Budget & Cash Flow

When looking at a purchase price for your investment, first determine what your maximum “Borrowing Capacity” is and then work out a comfortable figure below this level.

The weekly amount is more important than the purchase price. Quite simply, if you can not hold the asset for 10 years or through an entire property cycle, there is a higher chance that you will not get the desired result from your investment. If $200/week is your budget then you need to ensure that your investment property will cost you less than that figure each week after consideration of all expenses and benefits.

Your Property Investment Advisor can prepare a detailed cashflow analysis to show what this figure should be. You need to factor in:

On the outgoing side: Mortgage payments, Property management and letting costs, body corporate (or strata) fees, insurances, rates, annual charges, any other expenses

And the incoming: Rent and Tax benefits.

The balance is your cashflow figure.

Be comfortable with this and know how to work It our for each property you consider.

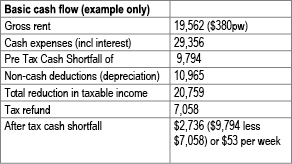

See the following example of a basic cash flow calculation.

In this example for just $53.00 per week or for the cost of 12 coffees a week you could own an investment property:

*This example is for someone on taxable income of $80,000 or less. For someone on more than $80,000 after tax cash shortfall is less than the above.