Why our property market won’t crash

How many times have we heard that one recently?

2021 was a year like no other – prices boomed creating new records and as the value of Australia’s housing market skyrocketed, the collective wealth of homeowners jumped by over $2 trillion despite the pandemic.

We have now moved into the next phase of the property cycle – the adjustment phase – and we won’t see the same level of overall price growth in 2022.

In fact, the value of some properties will fall, and certain sectors of the housing market will suffer, while other submarkets in certain States will do well.

Interest rates are going to keep rising for some time yet and this will cause hardship for some homeowners and property investors.

But I do not think we will be having a housing market crash.

Interest rates are only one of the many factors that affect home prices.

It is critical that you understand:

For a property market to “crash” there must be forced sellers and nobody on the other side of the transaction to purchase their properties, meaning they must give away their properties at very significant discounts.

Remember home sellers are also homebuyers – they must live somewhere. The only reason they would be forced to sell and give up their home would be if they were not able to keep up their mortgage payments.

This happens when:

- unemployed levels are high – today our unemployment is low.

- mortgage costs (interest rates) go up – despite rising interest rates, it was only a couple of years ago before the pandemic that rates were higher, borrowers could cope then.

Property prices will fall 30%

That was a recent headline in the Australian financial review by a respected columnist, and here he was not talking about a specific segment of the market, but about “the Australian property market.”

The fact is a property price drop of this magnitude has never happened before. Let may state that again – that has never ever happened before not during:

- the recession of the 1990s,

- the global financial crisis, and

- the stock market dive of 2017.

And considering the current state of the economy, our financial health and property markets there’s no credible reason to suggest a fall of this size should happen now.

1. The average Australian is wealthier than ever

CBA economists estimate that during lockdowns households have put away some $230 billion in excess savings.

Not only does the average Australian have significant savings, but surging property prices also means many homeowners have 30% more equity in their homes than they had 2 years ago.

Combine these 2 things with a strongly performing superannuation and shares portfolio (sure share prices have slumped a little lately) and the average Australian is now wealthier than ever.

So even if some homeowners do begin to struggle to make mortgage repayments or even default, the risk for Australia’s entire residential property market is still very low.

We also know from the recent Covid experience that the banks don’t want to take over your home in a mortgage default.

They will do whatever they can to help, including extending mortgage terms or giving mortgage repayment holidays.

2. No sign of mortgage stress for the majority of borrowers

There has been a lot of talk about the risk of mortgage stress but there is little evidence of this.

There are very few loan defaults as this stage.

Sure, some first home owners have overextended themselves and some investors have borrowed too much on the wrong properties but, in general, the percentage of borrowers in “real trouble” is low.

3. Interest rates are still low

Lower mortgage rates have been a significant driver of the property increase in prices seen over the past couple of years.

And sure Reserve Bank (RBA) governor, Philip Lowe, has warned us that more interest rate hikes are on the way, pledging not to repeat the costly mistakes of the 1970s stagflation period, and to “do what is necessary” to squash inflation before it becomes entrenched in the national psyche.

Lowe said inflationary pressures – ie the rising cost of living – were growing at a much faster pace than expected and the board had to act.

“High inflation damages the economy, reduces the purchasing power of people’s incomes and devalues people’s savings.

It is also regressive, hurting most those who are least well equipped to protect themselves.

So, it is important that we chart our way back to an inflation rate in the 2-3 per cent target range.

4. Banks are conservative with stress testing loans

When you borrow money, the bank or lender has a responsibility to ensure you have the financial capacity to service the mortgage repayments now and in the future.

Each bank and lender has its own stress test assessment based on the bank’s own appetite for risk, which is why your borrowing capacity can vary significantly from one lender to another.

On top of the assessment rate, the bank will also apply certain other factors and will load your existing (other) loans by a buffer, they account for all your incomes including wages and rental income(s), and they also include the limits on all of your credit cards.

The lender will also account for the number of financial dependants you have in your household, and apply a cost of living, which is the living amount used by the bank and may or may not be the same as what you and your household spend.

And if you’ve tried to borrow the money you’d know that the banks are incredibly conservative with stress testing loan applications.

That means that most mortgage owners who borrowed over the last couple of years will be able to handle the interest-rate increase of 2.5 or even 3%, and those who borrowed prior to these stricter requirements would have considerable equity in their properties.

5. Rising interest rates didn’t make the market fall in the past

This isn’t the first time we’re experiencing a period of rising interest rates.

Rates have risen before and it didn’t make the property market crash then, so why would it now?

Interest rates rose strongly for a 6-year period from 2004 to 2008 and then again from 2010 to 11 after the Global Financial Crisis.

In most of those years that interest rates rose, property values also increased.

Economist Stephen Koukoulos wrote an insightful piece in Yahoo Finance explaining it’s actually quite rare for rate-hiking cycles to coincide with falling house prices.

He explained that not counting the current interest rate cycle, there have been four instances in the past 30 years where the RBA has implemented an interest-rate-hiking cycle:

- August 1994 to December 1994 – Cash rate up 275 basis points.

- November 1999 to August 2000 – Cash rate up 250 basis points.

- May 2002 to March 2008 – Cash rate up 300 basis points.

- October 2009 to November 2010 – Cash rate up 175 basis points.

In each one of these four cycles, house prices were flat or higher – both one and two years after the first-rate hike.

Five years after the first-rate hike in each cycle, house prices were on average around 40 per cent higher.

Looking at house prices five years after the last hike in the cycle, they were always higher, with an average gain of around 30 per cent.

It is also noteworthy that house prices recovered after the flat patch in the wake of the 2009-2010 cycle, to be 26.1 per cent higher five years after the last hike in that cycle.

You see… how a particular property performs depends on a combination of factors – of which interest rates are just one.

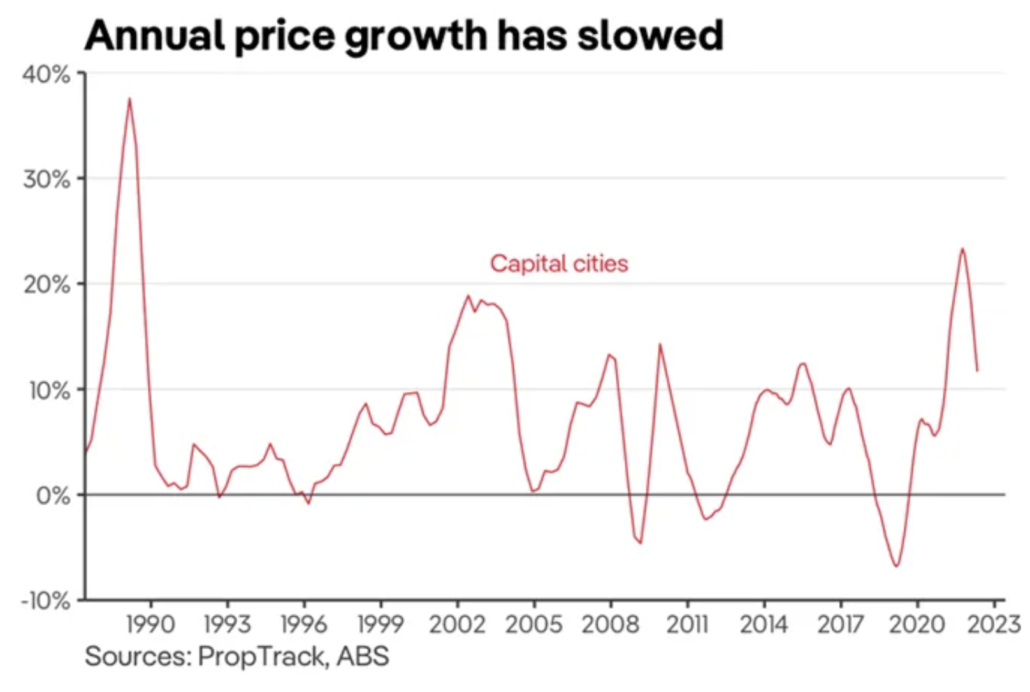

Australian property values have never “crashed” as the chart below shows

6. Dire supply shortage ahead

According to the latest National Housing and Finance Investment Corporation (NHFIC) state of the nation report, Australia could be in for a dire dwelling shortage ahead.

Data shows that while the housing supply may appear healthy in the short term, there is in fact a major supply crunch on the horizon.

This is particularly the case as net overseas migration recovers thanks to a newly opened border, the demand for new households will outstrip supply.

And such a supply shortage will act to put a floor under house price falls and only lead to increased prices going forward, with no property crash in sight.

7. Overseas migration is going to pick up

On the 21st of February 2022, the Australian Government opened Australian borders and welcomed double-vaccinated tourists and visa holders from around the world.

Eligible visa holders can come to Australia without a travel exemption or quarantining, and concessions are being granted to skilled visa holders in order to incentivise them to stay in the country for longer.

The latest overseas arrival data from the ABS shows total arrivals to Australia are starting to rise sharply as international students, permanent residents, and Australian citizens are welcomed back.

And those migration numbers are only expected to continue climbing.

As a result, we’re already seeing a pickup in demand in the rental market, once-abandoned central-city properties, and the unit market.

8. ‘Experts’ routinely get it wrong

It’s worth remembering that the same “experts” who are currently predicting that property markets will crash in 2023 are the same ones who have made multiple incorrect “Doomsday” predictions over the last couple of years.

Remember the Debt Bomb?

It didn’t explode.

Remember the fiscal cliff we were supposed to fall off?

That didn’t happen.

Unfortunately, these commentators have a track record of getting their property market predictions wrong, underestimating the strength and resilience of our housing markets.

9. Australia’s economy is strong

Economic activity in Australia contracted sharply in late 2021 due to the lockdowns associated with outbreaks of Covid-19’s Delta variant.

This setback delayed but not derailed the economic recovery that was underway in the first half of the year.

In fact, part of the reason we are experiencing inflation, and therefore rising interest rates, is because our economy is performing particularly well, and even though it will slow down over the next year, it will be supported by exports of fuel and food that will make a significant downturn unlikely.

As a country, Australia’s income will improve thanks to renewed tourist spending and also the Ukraine conflict.

That is because the Ukraine conflict, thanks to the disruption and threats to the supply of energy, industrial and agricultural commodities, and increased demand for metal-intensive defence goods, is providing a further boost to commodity prices.

This is particularly good news for commodity producers like Australia and further evidence of a strongly performing economy.

10. Australia is on the verge of a rental crisis

While the pace of house price growth has been slowing, rental growth has strengthened with vacancy rates around the country at the lowest they’ve been for a long, long time.

In fact, the nation is facing a chronic shortage of homes available for rent.

Similarly, a shortage of rental apartments is also developing, and will only get worse over the coming year.

Opening the international borders also has put additional strain on an already tight rental market.

Domain’s data shows that the national vacancy rate continued its downward trend, now at 1.1%, which is the lowest seen since Domain records began in 2017.

But these new figures are evidence yet again that we’re unlikely to see the property market crash.

While rental demand is surging and supply remains scarce, prices will only continue rising further, bringing more investors back into the market.

The bottom line.

So, there’s really no need to lose sleep or worry about the value of your home or investment property in the long term.

And if you’re not selling or refinancing in the short-term it doesn’t really matter if the value of your property drops 5% or so, does it?

Especially if it is appreciated 25 to 30% over the last couple of years.

We’re in the correction phase of the property cycle at present and there is no property crash in sight.

Whether it’s property, shares, or bitcoins — booms just don’t last forever, and neither do downturns.

So, think long-term and don’t seek quick wins.

And don’t listen to all those negative messages in the media.

It really doesn’t matter what the markets do in the short-term if you have sufficient financial buffers to ride out the storm.

And don’t let emotions drive your investment decisions, because it’s likely it will take a while for inflation to come under control and then the Reserve Bank will again start lowering interest rates because they always seem to exceed the mark.

We can help you achieve your goals and dreams. There are great opportunities around the Country but you must know where they are and how to lock them down. With our National Research and Acquisitions Team and our structured process we work with people to create long term wealth for them.

| Book a chat to find out more |